From

http://jessescrossroadscafe.blogspot.com/2009/06/some-common-fallacies-about-inflation.html

22 June 2009

There are several fallacies making the rounds of the economic

community, often put forward by pundits on the infomercials for

corporate America, and also on the internet among well-meaning but

badly informed bloggers.

The first of these monetary fallacies

is that 'the output gap will prevent inflation.' The second is that a

lack of net bank lending or other 'debt destruction' will require a

deflationary outcome. Let's deal with the output gap theory

first.

Output gap is the economic measure of the

difference between the actual output of an economy and the output it

could achieve when it is most efficient, or at full capacity.

The

theory is that when GDP underperforms its potential, with

unemployment remaining high, there can be no inflation because demand

is weak and median wages will be presumably stagnant. This idea comes

from neoliberal monetarist economics, and a misunderstanding of the

inflationary experience of the 1970s.

The thought is that

sustained inflation is due to a 'wage-price' spiral. Higher wages

amongst workers cause prices to rise, prompting workers to demand

higher wages, thereby fueling inflation. If workers do not have the

ability to demand higher wages there can be no inflation.

While

this is in part true, it tends to confuse cause and effect.

The cause of a monetary inflation, which is a broadly

based inflation across most products and services relatively

independent of demand, is often based in a monetary expansion of the

currency resulting in a debasement and devaluation.

A monetary expansion is relatively difficult to achieve under an

external standard since it must be overt and often deliberative. A

gradual inflation is an almost natural outcome under a fiat

currency regime because policy-makers can almost never resist

the temptation of cheap growth and the personal enrichment that comes

with it.

There can be short term non-monetary

inflation-deflation cycles that tend to be more product specific in a

market that is not under government price controls. But this is not

the same as a broad monetary inflation or deflation.

The key difference is the value of the dollar which has little or

nothing to do with a business cycle or product demand/supply induced

inflation/deflation.

In the modern era the Federal Reserve can

increase the money supply independent of demand by the monetization

of debt, with the only restrictions on their ability to increase

supply being the value of the dollar and the acceptability of US

sovereign debt. This requires the acquiescence of the Treasury and

the cooperation of at least one major money center bank.

People

tend to invent 'rules' about how the money supply is able to

increase, and confuse financial wagers and credit with money. This is

in part because the average mind rebels at the reality behind modern

currency and the ease at which it can be created. Further, people

often invent facts to support theories that they embrace in an a

priori manner.

In a pure fiat currency regime, the swings

between inflation and deflation are almost always the result of

policy decisions, with the occasional exogenous shock. A government

decides to inflate or strengthen their money supply relative to

productivity as a policy decision regarding spending, central bank

credit expansions, banking requirements and regulations, among other

things.

As a prime example of a rapid inflation despite a

severe economic slump, what one might call uber-stagflation,

is the Weimar experience.

Since pictures are worth 1000 words,

let me be brief by showing you a few important charts.

The basic ingredients of the Weimar experience are...

A high level of official debt issuance relative to

economic growth

High

unemployment with a slumping real GDP

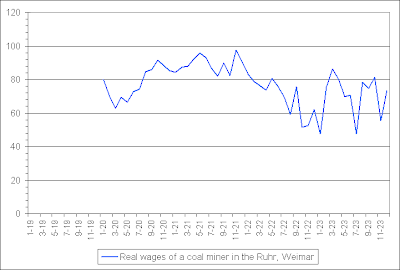

Wage

Stagnation

I

should stop here and note that although the statistics at hand

involve union workers, in fact unemployment was widespread in the

Weimar economy. The saving grace of being in the union was that one

was more often able to retain their jobs and some level of nominal

wage increases.

Anyone who has read the history of the times knows that unemployment,

underemployment and slack demand was rampant, and that hoarding was

commonplace as people refused to trade real goods for a rapidly

devaluing currency.

Rapidly Rising Prices Despite

Slack Demand and High Unemployment

So

much for the wage price spiral and the output gap.

A

Booming Stock Market, at Least in Nominal Terms

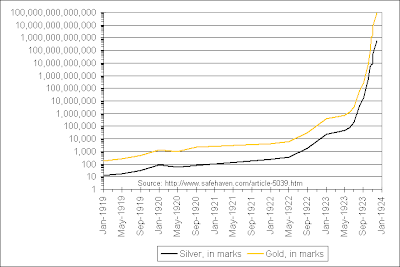

Booming

Price of Precious Metals as a Safe Haven Even While Basic

Material Prices Slumped

Notice the plunge in the price of copper as the economy collapsed

and gold and silver soared.

If

one can obtain a copy, as it is out of print, one of the best

descriptions of the German inflation experience is When Money

Dies: the Nightmare of the Weimar Collapse by Adam

Fergusson.

From my own readings in this area, the people who

tended to survive the Weimar stagflation the best were those who:

1.

Owned independent supplies of essentials including food and shelter

and were reasonably self-sufficient.

2. Had savings in foreign

currencies that were backed by gold such as the US dollar and the

Swiss Franc

3. Possessed precious metals

4. Belonged to a trade

union and/or had essential skills or government position which

guaranteed a wage

5. Were invested in foreign equity markets, and

even in the domestic German stock market for a time

People

will argue now that the Fed understands that inflation is caused by

perceptions, and that by managing those perceptions inflation can be

avoided because even those prices are rising and the currency is

being devalued, if they ignore it the inflation cannot reach harmful

levels.

People

will argue now that the Fed understands that inflation is caused by

perceptions, and that by managing those perceptions inflation can be

avoided because even those prices are rising and the currency is

being devalued, if they ignore it the inflation cannot reach harmful

levels.

This is what I call the "psychosis school"

of behavioral economics.

Granted, perception is

important, and managing perception may delay outcomes for a period of

time. But unless the underlying cause of the problem is remedied

during what is at best is an extended interlude, the resulting break

in perception will ignite a firestorm of cognitive dissonance, loss

of confidence, and social unrest.

In summary, in a purely fiat

currency regime a sustained monetary inflation or deflation is an

outcome of policy decisions regarding fiscal policy, monetary policy,

and economic balance and output.

As long as the government is able to generate debt, deflation is a

highly unlikely outcome. And when the government reaches the

practical limits of debt creation, the underpinnings of the currency

give way and the economy tends to collapse in a stagflationary

slump.

There are no predetermined outcomes. Deflation,

stagflation and hyperinflation are not 'normal' but are certainly

possible if the central authority is permitted to abuse the real

economy and the money supply for protracted periods of time.

What

about Japan? Japan is the perfect example of a policy decision made

by a fiat currency regime in what was decidedly NOT a free market,

but under the de facto control of a highly entrenched

bureaucracy, a single political party, and large corporate giants in

pursuit of an industrial policy that favored exports and domestic

deflation.

The difference between the Japan of the 1980s and

the US of today could not be more stark. Choosing a deflationary

policy and high interest rates as a debtor nation is economic and

political suicide. It would be interesting to see what happens if the

US elites try to take that path.

We will know if there is a

true monetary deflation in the US because the value of the dollar

will start increasing dramatically with regard to other hard assets,

other currencies, goods and services, and precious metals and

commodities. Prices will decline especially for imports as the dollar

gains in purchasing power.

Remember that a true monetary

inflation and deflation would only show up over time. Even in the

Great Depression in the US, as demand slumped and prices fell, the

stage was set for a significant devaluation of the US dollar and a

rise in consumer prices well in advance of the eventual recovery of

the economy that caused the Fed to tighten prematurely. As I recall

the actual contraction in money supply lasted two years. This again

highlights was [what?] an amazing piece

of bad policy that Japan represents in its 'lost decade.'

People

embrace beliefs for many motivations. So often I find they are not

'rational' and based on a scientific study of the facts, even on the

most cursory level. Fear and greed and prejudice are often

motivations that are surprisingly resilient, even in the face of

overwhelming evidence against them. Leadership understands this

well.

There are often appeals to private judgement. I do

not care what you say, this is what I believe, what I think, what I

feel. This is appropriate in the supra-natural realm, but in the

natural realm there may be private judgement but the facts are

public, and the outcomes are well beyond the complete control of the

most fully-managed perceptual campaigns, at least so far in human

experience.

"The lie can be maintained only for such time as

the State can shield the people from the political, economic and or

military consequences of the lie. It thus becomes vitally important

for the State to use all of its powers to repress dissent, for the

truth is the mortal enemy of the lie, and thus by extension, the

truth is the greatest enemy of the State." Joseph Goebbels,

of the perception modification school of economic thought

What is truth? It is difficult to estimate but not completely

out of reach.

Our own view is that a serious stagflation with further

devaluation of the US dollar as it is replaced as the world's reserve

currency is very likely, after a period of slackening demand and high

unemployment. A military conflict is also a probable outcome as

countries often go to war when they fail at peace.

Weimar was not an anomaly although the level of inflation was

indeed legendary. Argentina, post Soviet Russia, and most recently

Zimbabwe are all similar examples. Serious

Instances of Monetary Inflation Since World War II

There

are many, many variables in play here, and policy decisions yet to be

made. It is highly discouraging to see Obama's

Administration fail so miserably to do the right things, but

there is always room for hope, less so today than six months ago

however.

Argue and shout grave oaths and wave our hands though

we might, we are in God's hands now.

Let's see what

happens.

A very special thanks to our friend Bart at Now

and Futures who makes these charts, among other

things, available on his highly informative web site for public

review. If you are not familiar with his work you might do well to

view it. We do not always agree, but he demands attention because of

the rigor which he applies to his work for which we are grateful,

always.

Posted by Jesse at 2:19

PM